Unified Payments Interface (UPI) was launched in India in April 2016 by the National Payments Corporation of India (NPCI) as a game-changer in the country’s digital payment landscape. It was developed to facilitate real-time UPI UTR Numbers Explained and Features and Benefits money transfers between bank accounts using a mobile device. UPI aims to simplify transactions, making them accessible to the masses, regardless of their financial literacy. The introduction of UTR numbers was a strategic move to enhance transparency and accountability in this new system.

Initially, digital payments were marred by concerns over security, complexity, and accessibility. Traditional banking methods were often slow, UPI UTR Numbers Explained and Features and Benefits involving multiple steps, which made them less appealing for everyday use. UPI was designed to overcome these challenges, allowing users to send and receive money instantly using their smartphones. The introduction of UTR numbers further bolstered UPI’s efficiency by providing a reliable means of tracking each transaction.

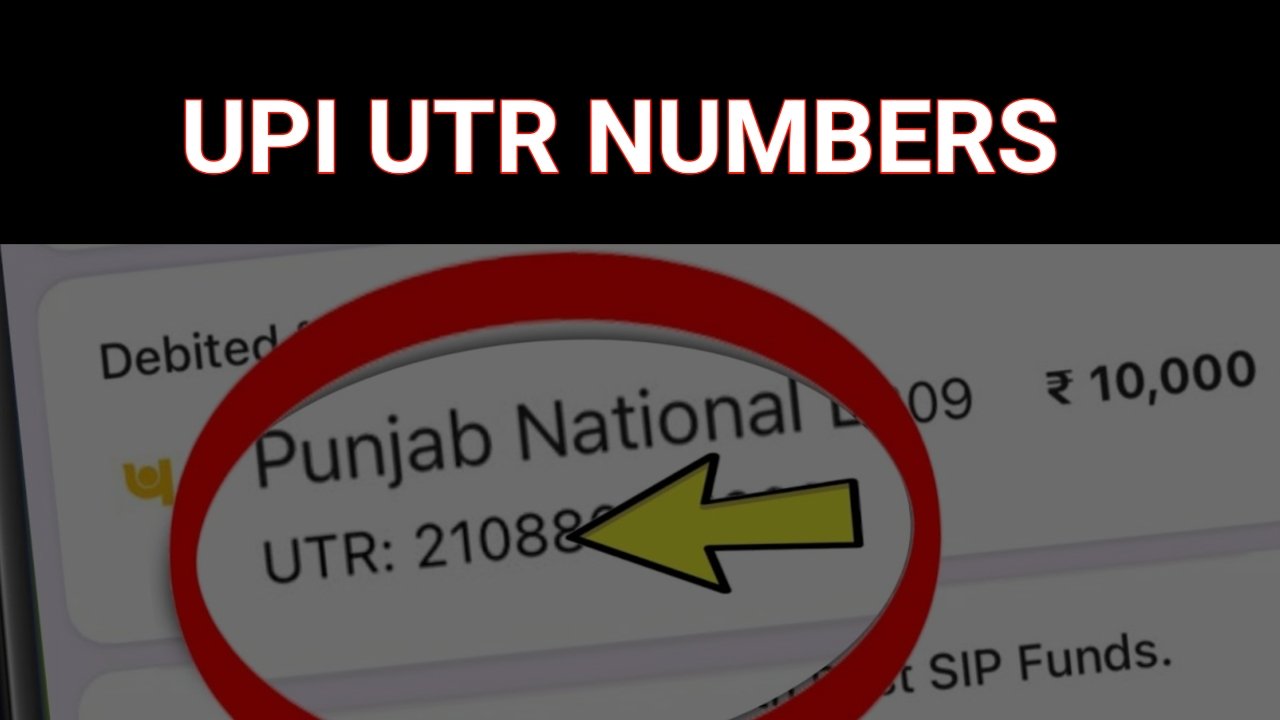

UPI UTR Numbers Explained and Features and Benefits

In the broader context of digital transactions, UTR numbers play a pivotal role in ensuring that the UPI ecosystem functions smoothly. The simplicity of UPI is one of its primary draws, and the addition of UTR numbers aids in maintaining this simplicity. By assigning a unique identifier to each transaction, UTR numbers allow users to engage with their financial activities confidently.

Moreover, UTR numbers are not just beneficial for individual users; they also contribute significantly to the operational efficiency of banks and payment service providers. When a transaction occurs, the UTR number allows these entities to reconcile their accounts quickly. In the case of any discrepancies, the UTR can serve as a point of UPI UTR Numbers Explained reference, enabling banks to track the transaction flow seamlessly.

Practical Applications of UPI UTR Numbers

1. Personal Financial Management

For individuals managing their finances, the UTR number is invaluable. UPI UTR Numbers Explained Users can easily keep track of their spending, categorize transactions, and analyze their financial habits over time. Many personal finance apps and budgeting tools allow users to input UTR numbers to track specific payments, making it easier to manage expenses.

2. Small Businesses and Entrepreneurs

Small businesses benefit significantly from UPI UTR numbers. For instance, when a customer makes a payment through UPI, the business can instantly generate an invoice that includes the UTR number. This practice not only serves as a proof of payment but also enhances the customer experience by providing transparency in transactions. Additionally, small businesses can use UTR numbers to keep track of payments received UPI UTR Numbers Explained and streamline their accounting processes.

3. E-commerce and Online Transactions

With the rise of e-commerce, UTR numbers have become critical in managing online transactions. E-commerce platforms often integrate UPI payment gateways, allowing customers to pay seamlessly. The inclusion of UTR numbers in payment confirmations reassures customers that their transactions are secure and can be tracked. For e-commerce businesses, having access to UTR numbers helps in resolving customer queries about payment status, thereby enhancing customer satisfaction.

4. Educational Institutions and Utility Payments

Educational institutions and utility companies have adopted UPI payments for fee payments and bill settlements. By using UTR numbers, these institutions can easily track payments from students or customers. The UTR serves as a confirmation of payment, making the process transparent and efficient. For instance, students can easily reference their UTR numbers if they need to verify payments or address discrepancies with their institutions.

Security Aspects of UPI and UTR Numbers

With the increasing digitization of financial transactions, security remains a top concern for users. The UPI system, including UTR numbers, has built-in security features designed to protect users from fraud and unauthorized transactions.

1. Two-Factor Authentication (2FA)

UPI transactions typically require two-factor authentication, meaning that users must authenticate their identity through an additional method beyond just their mobile device. This could include a PIN or biometric verification. UTR numbers enhance this security by acting as a unique transaction identifier, helping banks trace any suspicious activity.

2. Encryption Protocols

UPI systems employ advanced encryption protocols to protect user data during transactions. This encryption ensures that UTR numbers and other sensitive information are transmitted securely, reducing the risk of interception by malicious actors.

3. User Awareness

Educating users about the importance of keeping their UTR numbers confidential is essential. Users should be advised not to share their UTR numbers publicly or with unverified sources to prevent unauthorized access to their accounts. Awareness campaigns by banks and financial institutions can play a vital role in enhancing user security.

The Future of UPI UTR Numbers

As India moves towards a more digitized economy, the role of UPI and UTR numbers is expected to expand further. Here are some anticipated trends and developments:

1. Integration with International Payment Systems

As Indian businesses look to expand globally, the integration of UPI with international payment systems could enhance its usability for cross-border transactions. This development may also include the assignment of UTR-like identifiers for international transactions, making it easier to track and manage payments across borders.

2. Enhanced User Experience through Technology

The future may see advancements in user interfaces and experiences when managing UTR numbers. Innovative technologies such as Artificial Intelligence (AI) and Machine Learning (ML) could facilitate better transaction categorization and tracking, UPI UTR Numbers Explained allowing users to gain insights into their spending patterns.

3. Broader Financial Inclusion

The continued promotion of digital payments, including UPI and UTR numbers, can drive financial inclusion, particularly in rural and semi-urban areas. With increasing smartphone penetration and internet access, more people can engage in digital transactions, helping to bring unbanked populations into the financial system.

4. Regulatory Frameworks and Consumer Protection

As UPI and its associated features grow, so will the need for robust regulatory frameworks. Regulatory bodies may implement stricter guidelines to protect consumers and ensure fair practices in digital transactions. This could include measures for dispute resolution, ensuring that UTR numbers are used responsibly and ethically.

As we embrace the future of digital finance, the UPI UTR number stands as a testament to the innovative strides being made in creating a more transparent, efficient, and accessible payment system for all. With growing awareness and education around these systems, users can confidently navigate the digital payment landscape, leveraging the benefits of UPI and UTR numbers to enhance their financial experiences.

Importance of UTR Number in UPI Transactions

In the modern digital payment landscape, UPI (Unified Payments Interface) has emerged as a groundbreaking platform, allowing users to conduct seamless and instantaneous financial transactions. Central to the functioning of UPI is the Unique Transaction Reference (UTR) number. This alphanumeric code serves as an essential element in tracking transactions, resolving disputes, and ensuring the overall integrity of the payment process. In this article, we will delve into the significance of the UTR number, its role in transaction tracking, and its utility in resolving payment issues, demonstrating its critical importance in the UPI ecosystem.

What is a UTR Number?

A UTR number is a unique identifier assigned to each UPI transaction processed through the payment system. This reference number is generated at the time of the transaction and is typically a combination of letters and numbers. The UTR serves various functions, including tracking the transaction status, verifying payment details, and facilitating communication between banks and payment service providers. Understanding the importance of UTR is crucial for anyone engaged in UPI transactions, whether for personal or business purposes.

Role in Transaction Tracking

The UTR number plays a vital role in transaction tracking, offering a straightforward method for users to monitor their financial activities. Here are several ways in which the UTR number aids in transaction tracking:

- Real-Time Monitoring: One of the primary advantages of UPI is its ability to provide real-time transaction updates. Users can view their transaction history on their banking apps or UPI-enabled applications. The UTR number allows them to identify specific transactions, making it easier to track spending patterns and maintain financial records.

- Verification of Transaction Status: The UTR number can be used to verify the status of a transaction. Users can check whether a payment has been successful, pending, or failed by entering the UTR number into their banking app or contacting their bank’s customer service. This functionality provides users with peace of mind, knowing they can confirm the status of their transactions at any time.

- Facilitating Refunds and Reversals: In cases where a transaction needs to be reversed or refunded, the UTR number is crucial. Users can provide the UTR to their bank or payment service provider, enabling them to quickly locate the transaction in their records and initiate the refund process. This efficiency is essential in maintaining customer satisfaction and trust in digital payment systems.

- Audit and Compliance: For businesses, the UTR number serves as an essential tool for auditing and compliance purposes. Organizations can track their transactions through UTR numbers, ensuring they maintain accurate financial records and comply with regulatory requirements. This is particularly important for businesses that must adhere to stringent financial regulations.

- Enhanced Security: The use of UTR numbers contributes to the security of transactions. Since each transaction has a unique identifier, it becomes difficult for unauthorized users to manipulate or replicate transactions. In the event of fraud or disputes, the UTR number provides a clear trail of transaction history, aiding in investigations.

- Integration with Financial Management Tools: Many users rely on financial management tools and budgeting apps to keep track of their finances. The UTR number enables seamless integration of transaction data into these applications. Users can easily import their UPI transactions, categorized by UTR numbers, into their financial management tools, facilitating better financial planning and budgeting.

- Enabling Cross-Border Transactions: As UPI gains popularity beyond India’s borders, particularly with initiatives like UPI Link for international payments, the UTR number will be essential in tracking cross-border transactions. This becomes particularly significant in ensuring compliance with international financial regulations and preventing fraudulent activities across different jurisdictions.

- Record Keeping for Tax Purposes: For individuals and businesses alike, maintaining accurate financial records is crucial for tax reporting. The UTR number serves as an important reference when compiling financial statements or tax returns. Users can retrieve transaction histories using UTR numbers to ensure that all income and expenses are accurately reported, helping avoid potential tax complications.

Use for Resolving Payment Issues

Despite the efficiency of UPI transactions, users may occasionally encounter payment issues such as failed transactions, discrepancies in amounts, or delayed credits. The UTR number becomes an invaluable asset in resolving these payment-related challenges. Here’s how:

- Identifying and Reporting Issues: When users face payment issues, the UTR number helps them pinpoint the specific transaction that caused the problem. Users can contact their bank or payment service provider with the UTR number, allowing customer service representatives to quickly access transaction details. This identification is crucial in addressing user concerns swiftly.

- Expedited Dispute Resolution: In cases of disputes, the UTR number simplifies the resolution process. Users can refer to the UTR when discussing issues with their banks or payment service providers. This reference eliminates confusion and miscommunication, allowing for quicker resolution. Financial institutions can access transaction logs and provide accurate information based on the UTR, ensuring that disputes are handled efficiently.

- Tracking Delayed Payments: In scenarios where payments are delayed, the UTR number can be used to track the transaction through the banking network. Users can inquire about the status of their payment and obtain updates on any potential delays. This transparency is critical in maintaining trust between users and service providers, as it demonstrates that the financial institution is actively working to resolve the issue.

- Providing Evidence for Fraud Claims: In unfortunate cases of fraud or unauthorized transactions, the UTR number serves as evidence of the transaction. Users can present the UTR to their banks when filing fraud claims, offering a clear record of the transaction that can be investigated. This evidence is vital in ensuring that users receive the necessary support and that any fraudulent activity is dealt with promptly.

- Establishing Accountability: The UTR number establishes accountability within the payment ecosystem. By linking each transaction to a unique identifier, it becomes easier for financial institutions to monitor transactions, detect irregularities, and implement corrective measures. This accountability is essential for maintaining the integrity of the UPI system and fostering user confidence.

- Facilitating Communication Between Banks: In many cases, transactions may involve multiple banks or payment service providers. The UTR number streamlines communication between these entities. When users report issues, the UTR number enables banks to collaborate effectively, share transaction data, and resolve issues collaboratively. This cooperative approach is vital in a multi-bank environment, where smooth communication is essential for user satisfaction.

- Preventing Duplicate Transactions: Occasionally, users may initiate a payment multiple times due to uncertainty about the transaction’s status. The UTR number helps in preventing duplicate transactions, as banks can check the transaction logs using the UTR. This capability not only saves users from unnecessary charges but also helps maintain the integrity of their financial records.

- User Education and Empowerment: Understanding the significance of the UTR number empowers users to take control of their financial transactions. Educating users about how to utilize UTR numbers can reduce anxiety associated with digital transactions and build confidence in using UPI for their financial needs. This education can lead to a more informed user base that can navigate financial transactions effectively.

The UTR number not only enhances the user experience by providing real-time insights into transactions but also establishes accountability within the payment ecosystem. By fostering transparency and communication between financial institutions, the UTR number contributes to a robust and reliable digital payment infrastructure. As the adoption of UPI grows, so too will the significance of the UTR number in ensuring secure, efficient, and user-friendly financial transactions.

The evolution of UPI and the reliance on UTR numbers underscore a shift towards a more accountable and transparent financial ecosystem. As digital transactions become an integral part of everyday life, the UTR number stands as a testament to the importance of maintaining clarity and security in financial dealings.

The Future of UTR Numbers in UPI Transactions

Looking ahead, the role of UTR numbers is poised to expand further with advancements in technology and changes in consumer behavior. As more people embrace digital payments, the need for effective tracking and resolution mechanisms will only intensify. Here are a few potential future trends regarding UTR numbers in UPI transactions:

- Integration with Blockchain Technology: As the financial industry explores blockchain technology, the integration of UTR numbers with blockchain could enhance transaction transparency and security. Each transaction recorded on a blockchain can be tracked and verified, potentially making UTR numbers even more powerful as identifiers in this evolving landscape.

- Use in Smart Contracts: The emergence of smart contracts could lead to new applications for UTR numbers. By tying UTR numbers to smart contracts, automated processes could be established for payments, refunds, and dispute resolution, making the entire transaction process more efficient and reliable.

- Enhanced User Experience through AI: The use of artificial intelligence (AI) in financial services is on the rise. AI algorithms could analyze transaction data linked to UTR numbers to provide personalized insights, alerts, and recommendations to users, enhancing their financial management capabilities.

- Global Adoption and Standardization: As UPI expands its reach globally, standardizing the use of UTR numbers across different jurisdictions could help establish a consistent and reliable framework for international transactions. This could facilitate smoother cross-border payments and encourage more users to adopt digital payment systems.

- Greater Regulatory Oversight: With the increasing scrutiny of digital payment systems, regulatory authorities may require enhanced reporting and tracking mechanisms.

to ensure consumer protection and fraud prevention. The UTR number could play a significant role in meeting these regulatory requirements, providing a clear audit trail for transactions that can be reviewed by authorities when necessary. This enhanced oversight can foster consumer trust and confidence in UPI systems, encouraging more widespread adoption of digital payments.

- Improved Dispute Resolution Mechanisms: Future developments may see the implementation of more sophisticated dispute resolution systems that leverage UTR numbers. With advanced algorithms and data analytics, financial institutions could quickly assess transaction histories and discrepancies, leading to faster resolutions for customers. This capability could minimize the stress and uncertainty associated with payment issues.

- Greater Focus on Consumer Education: As UPI continues to grow, educational initiatives focusing on UTR numbers will be essential. Banks and payment service providers might offer workshops, online resources, and tutorials to help consumers understand the significance of UTR numbers and how to use them effectively. A well-informed user base is likely to experience fewer issues and engage more confidently with digital payment platforms.

- Integration with Other Financial Services: As digital payment platforms evolve, UTR numbers may become integrated with various financial services, including budgeting tools, investment platforms, and personal finance management applications. By linking UTR numbers to a comprehensive financial overview, users could gain deeper insights into their spending habits and overall financial health.

- Increased Customization of UTR Formats: To accommodate the diverse needs of users and financial institutions, there may be a push for customizing UTR formats. This flexibility could allow different banks to develop UTR structures that suit their specific requirements while still maintaining the core functionality of a unique identifier for transactions.

- Adoption of UTR-like Systems in Other Payment Methods: The success and effectiveness of UTR numbers in UPI transactions may inspire similar systems in other payment methods. Credit card transactions, mobile wallets, and even traditional bank transfers could incorporate unique reference numbers to enhance tracking and dispute resolution capabilities across various platforms.

As we embrace the future of financial transactions, the importance of UTR numbers in UPI transactions will only increase, emphasizing the need for users to stay informed and engaged with their financial dealings. Whether for personal use, business transactions, or cross-border payments, the UTR number is an essential tool that empowers users to navigate the complexities of digital payments with ease and confidence.

By understanding and leveraging the power of UTR numbers, users can take control of their financial transactions, ensuring that they are equipped to handle any challenges that may arise in the ever-evolving digital payment landscape. This knowledge not only enhances individual financial literacy but also contributes to a more robust, transparent, and trustworthy financial ecosystem as a whole.

Understanding UPI and UTR

Unified Payments Interface (UPI) has revolutionized the way transactions are conducted in India. One critical aspect of UPI transactions is the Unique Transaction Reference (UTR) number. This number serves as a unique identifier for each transaction, helping users and banks trace and verify transactions. Knowing how to locate the UTR number can be essential, especially for tracking payments, resolving disputes, or confirming transactions.

Checking UTR in UPI Apps

Most UPI apps provide an easy way to view transaction details, including the UTR number. Here’s how to find it using various popular UPI applications:

1. Using Google Pay

- Step 1: Open the Google Pay app on your mobile device.

- Step 2: Go to the “Activity” section, where all your transactions are listed.

- Step 3: Find the transaction for which you need the UTR number. Tap on it to see the details.

- Step 4: Scroll down, and you should see the UTR number displayed alongside other details like transaction ID, date, and amount.

2. Using PhonePe

- Step 1: Launch the PhonePe app.

- Step 2: Tap on the “History” option at the bottom of the screen.

- Step 3: Browse through the list to find your transaction.

- Step 4: Click on the transaction, and the UTR number will be shown in the transaction details section.

3. Using Paytm

- Step 1: Open the Paytm app.

- Step 2: Go to the “Passbook” option, which contains your transaction history.

- Step 3: Locate the specific transaction and tap on it.

- Step 4: The UTR number will be displayed among the transaction details, making it easy to reference.

4. Using BHIM App

- Step 1: Open the BHIM app on your phone.

- Step 2: Navigate to the “Transactions” section.

- Step 3: Find and select the transaction you’re interested in.

- Step 4: The UTR number will appear on the transaction detail screen.

Advantages of Accessing UTR via UPI Apps

Accessing the UTR number through UPI apps is quick and efficient. The user-friendly interfaces of these apps allow users to easily navigate their transaction history. Additionally, since UPI transactions are updated in real-time, you can find the UTR number immediately after the transaction is completed. This instant access helps in prompt resolution of payment-related queries and aids in financial tracking.

Locating UTR in Bank Statements

If you cannot find your UTR number through your UPI app, another reliable way to access it is through your bank statements. Most banks will include UTR numbers in transaction summaries. Here’s how to locate it:

1. Using Online Banking

- Step 1: Log in to your bank’s online banking portal.

- Step 2: Navigate to the “Accounts” or “Statements” section.

- Step 3: Select the account linked with your UPI transactions.

- Step 4: Look for the option to view your recent transactions or statements.

- Step 5: Once you access your statements, find the specific UPI transaction. The UTR number is typically included in the transaction details along with the date, amount, and transaction type.

2. Using Mobile Banking Apps

Most banks have mobile banking apps that you can use to view your account statements:

- Step 1: Open your bank’s mobile banking app.

- Step 2: Log in with your credentials.

- Step 3: Access the “Transaction History” or “Account Statements” section.

- Step 4: Locate the UPI transaction of interest. The UTR number should be listed alongside the transaction details.

3. Physical Bank Statements

If you prefer physical copies, you can request a printed bank statement from your bank. Here’s how to go about it:

- Step 1: Visit your bank branch and request your account statement for a specific period.

- Step 2: Once you receive the statement, look for your UPI transaction entries.

- Step 3: The UTR number will be listed with other transaction details.

Understanding UTR in Bank Statements

The UTR number in bank statements usually appears as a long alphanumeric string. It is essential for:

- Dispute Resolution: If a transaction fails or an amount is debited without a successful transaction, the UTR number helps in tracing the transaction for resolution.

- Financial Record-Keeping: Individuals and businesses can maintain accurate records of transactions for budgeting and financial planning.

Understanding UPI UTR and Other Transaction IDs

In today’s digital world, financial transactions have become increasingly efficient and convenient, largely thanks to the evolution of payment systems. One of the most notable advancements is the Unified Payments Interface (UPI), which has revolutionized how people make payments in India. However, with this convenience comes the necessity for effective tracking and identification of transactions. This is where various transaction IDs come into play, particularly the UPI Unique Transaction Reference (UTR) number, Transaction Reference Number (TRN), and Payment ID. Understanding the differences between these identifiers is crucial for anyone navigating the landscape of digital payments.

What is UPI?

The Unified Payments Interface (UPI) is a real-time payment system developed by the National Payments Corporation of India (NPCI). It facilitates seamless money transfers between bank accounts via mobile devices. UPI enables users to link multiple bank accounts to a single mobile application, making transactions easy and quick. UPI transactions can be made using a UPI ID or mobile number, ensuring user-friendly access to digital payments. Each transaction processed through UPI is assigned a unique identifier known as the UPI UTR.

What is a UPI UTR?

The UPI UTR (Unique Transaction Reference) number is a unique identifier generated for every transaction made through the UPI platform. It serves as a reference that allows users and banks to track and verify specific transactions. The UTR number typically consists of a combination of alphanumeric characters that provide a traceable pathway back to the transaction.

Key Features of UPI UTR:

- Uniqueness: Each UPI transaction receives a distinct UTR number, ensuring that every payment can be easily tracked.

- Tracking: Users can utilize the UTR number to track the status of their payments, whether successful, pending, or failed.

- Verification: In cases of disputes or errors, the UTR number serves as an essential piece of information for customer support and bank representatives.

What is a Transaction Reference Number (TRN)?

The Transaction Reference Number (TRN) is another type of unique identifier used in various financial systems to track transactions. While it serves a similar purpose to UTR, the context in which it is used can differ significantly. TRNs are often associated with multiple types of transactions, including but not limited to card payments, online banking, and wire transfers.

Key Features of TRN:

- Versatility: TRNs can be used across various banking and financial services, not just UPI transactions.

- Format: The structure of a TRN may vary depending on the financial institution and the type of transaction. Unlike UTRs, which follow a specific format under UPI, TRNs may have differing lengths and character compositions.

- Tracking Capability: Like UTR, the TRN allows users and financial institutions to track the progress and status of a transaction, aiding in the identification of issues.

UTR vs. TRN: Key Differences

While both UTR and TRN serve as unique identifiers for transactions, there are notable differences between the two:

- Scope of Use:

- UPI UTR: Exclusively used within the UPI ecosystem for transactions executed via the UPI platform.

- TRN: Utilized across various banking platforms and transaction types, making it more versatile in terms of application.

- Format and Structure:

- UPI UTR: Typically adheres to a specific alphanumeric format defined by the NPCI.

- TRN: The format can vary widely based on the financial institution and the specific service being used.

- Transaction Type:

- UPI UTR: Specifically linked to mobile transactions made through UPI.

- TRN: Can be assigned to various transactions, including card payments, electronic fund transfers, and more.

- Tracking and Verification:

- Both UTR and TRN enable tracking and verification, but the UTR is specifically tailored for the UPI framework, providing seamless integration with UPI-based apps and services.

What is a Payment ID?

A Payment ID is another important identifier in the realm of digital transactions. It is often used in different payment gateways and platforms to track transactions. Unlike UTRs and TRNs, which are more closely related to banking systems, Payment IDs are frequently utilized in e-commerce platforms, online payment gateways, and mobile wallets.

Key Features of Payment ID:

- Purpose: Payment IDs are primarily used to identify transactions made through specific payment gateways, often facilitating refunds or cancellations.

- Integration with E-Commerce: Many e-commerce platforms generate unique Payment IDs for transactions, allowing merchants and customers to track orders efficiently.

- Format: The structure of a Payment ID can vary significantly across platforms, much like TRNs.

UTR vs. Payment ID: Key Differences

When comparing UTR with Payment IDs, several distinctions emerge:

- Usage Context:

- UPI UTR: Used within the UPI framework and is primarily linked to bank transactions.

- Payment ID: Utilized in the context of e-commerce transactions and payment gateways, making it more relevant for online shopping.

- Issuing Authority:

- UPI UTR: Generated by the banking institution handling the UPI transaction.

- Payment ID: Typically generated by the e-commerce platform or payment gateway facilitating the transaction.

- Tracking Scope:

- UPI UTR: Helps in tracking transactions directly with the bank or through UPI apps.

- Payment ID: Assists in tracking order status and transaction history on e-commerce platforms, which may not directly link back to a bank account.

- Transaction Types:

- UPI UTR: Strictly related to transactions conducted via the UPI interface.

- Payment ID: Can cover a broader range of transaction types, including purchases made through online shopping carts, subscriptions, and digital services.

Uses of UTR Number in Payment Disputes

In the world of digital transactions, the Unique Transaction Reference (UTR) number serves as a critical identifier that simplifies tracking and managing payments. This unique alphanumeric code is generated for every transaction processed through electronic payment systems, including bank transfers, online purchases, and remittances. UTR numbers are vital in various situations, particularly when it comes to resolving payment disputes. This article will delve into the two primary uses of UTR numbers in payment disputes: reporting failed transactions and claiming refunds.

Reporting Failed Transactions

When consumers engage in online transactions, they expect the process to be seamless and reliable. However, issues such as technical glitches, network failures, or discrepancies in transaction details can lead to failed payments. A failed transaction is typically characterized by a lack of successful completion, resulting in debited funds from the sender’s account without a corresponding credit to the recipient. In such scenarios, reporting the issue promptly is crucial to ensure the funds are traced and returned.

The UTR number plays a pivotal role in reporting failed transactions. When a customer notices that a transaction has failed, the first step is to gather relevant information, including the UTR number. This unique reference acts as a crucial identifier that helps banks and payment service providers trace the transaction quickly. By providing the UTR number to the customer service representative, the user can streamline the dispute process.

Moreover, banks often require the UTR number to initiate an investigation into the failed transaction. The UTR acts as a digital fingerprint for the transaction, allowing the bank to access detailed records related to the payment attempt. This information typically includes the transaction amount, timestamps, sender and recipient details, and the reason for failure, if available. Consequently, having the UTR number readily available can significantly expedite the resolution process, reducing the overall time taken to address the issue.

In addition to expediting investigations, reporting failed transactions with the UTR number ensures a more organized approach to dispute resolution. Financial institutions maintain detailed logs of all transactions, and referencing the UTR allows for efficient tracking of inquiries and resolutions. This traceability also aids in analyzing patterns of failed transactions, helping banks improve their services and reduce the occurrence of such issues in the future.

It’s essential for customers to remain vigilant and proactive when dealing with failed transactions. After reporting the issue and providing the UTR number, customers should follow up with their banks regularly to receive updates on the status of their dispute. Keeping a record of communication, including names of representatives spoken to and timestamps of interactions, can be beneficial if further escalation is needed. By understanding the importance of the UTR number in reporting failed transactions, consumers can take a more informed and effective approach to resolving payment disputes.

Claiming Refunds Using UTR Number

Another significant use of the UTR number in payment disputes is for claiming refunds. In various situations, consumers may find themselves needing to request a refund for a transaction. This could be due to reasons such as receiving the wrong item, a service not being delivered, or even changes in purchase decisions. Regardless of the reason, the UTR number remains a critical component in facilitating the refund process.

When initiating a refund request, customers should always provide the UTR number associated with the original transaction. This helps the merchant or payment processor quickly identify the payment and verify its details. In many cases, refund policies may stipulate that customers include the UTR number to streamline processing. By ensuring that this information is provided upfront, customers can avoid unnecessary delays in receiving their refunds.

The process of claiming a refund typically involves submitting a formal request to the merchant or service provider. Depending on the merchant’s policies, this request may need to be made through an online form, email, or customer service call. In each instance, the UTR number serves as a point of reference that enhances the accuracy and efficiency of the request. It allows the merchant to cross-check their records and confirm the transaction before proceeding with the refund.

In addition to expediting the refund process, the UTR number can also provide an additional layer of protection for consumers. In instances where disputes arise over the legitimacy of a refund claim, having a UTR number readily available can help verify the transaction’s authenticity. This is especially useful in cases where there may be confusion over the nature of the transaction or if the merchant questions the request’s validity.

Moreover, using the UTR number in refund claims facilitates better record-keeping for both consumers and businesses. Consumers can maintain a detailed record of their transactions, including the UTR numbers for purchases. This practice helps track spending patterns and manage finances effectively. On the business side, having accurate UTR information aids in reconciling accounts and managing refunds efficiently.

It is important to note that refund processing times can vary based on the merchant and payment processor. While some refunds may be processed immediately, others might take several business days to reflect in the customer’s account. By using the UTR number, customers can inquire about the status of their refunds if delays occur, making it easier to resolve any potential issues.

How UPI UTR Number Helps in Fraud Detection

The Unified Payments Interface (UPI) has transformed digital transactions in India, providing a seamless way to send and receive money. One of the critical components of UPI transactions is the UTR (Unique Transaction Reference) number, a unique identifier assigned to each transaction. This number plays a significant role in fraud detection and prevention by facilitating tracking, verification, and accountability. In this article, we will explore how the UPI UTR number assists in fraud detection, focusing on two main areas: tracking suspicious transactions and verifying payments.

Tracking Suspicious Transactions

The ability to track transactions is crucial for identifying and preventing fraud. The UTR number enables financial institutions and users to trace each transaction in detail, which is vital for several reasons.

- Immediate Access to Transaction Data

Each UPI transaction generates a unique UTR number that is recorded in the financial institution’s system. This number provides immediate access to transaction details, including the sender and receiver’s information, transaction amount, date, and time. Financial institutions can quickly retrieve this data to monitor transactions for unusual patterns or discrepancies. - Identifying Unusual Patterns

By analyzing transactions using UTR numbers, banks and payment platforms can identify unusual patterns that may indicate fraudulent activities. For instance, if a user typically transacts small amounts and suddenly initiates a large transaction to an unknown recipient, this could trigger an alert. The UTR number allows banks to isolate these transactions for further investigation. - Historical Transaction Analysis

The UTR number also facilitates historical transaction analysis. Financial institutions can review past transactions associated with a specific UTR to determine whether a pattern of suspicious behavior exists. For instance, if multiple transactions with similar characteristics are flagged within a short period, it may indicate a coordinated fraudulent scheme. - User Reports and Verification

If a user suspects fraud, they can report the suspicious transaction to their bank, providing the UTR number. This number allows the bank to quickly access the transaction details and initiate an investigation. User reports combined with UTR tracking create a robust system for identifying potential fraud. - Collaboration Between Institutions

The UTR number standardizes transaction tracking across different banks and payment platforms. This standardization allows for collaboration between financial institutions when investigating fraud. If a transaction is flagged by one bank, the UTR number can be shared with other institutions involved in the transaction for further analysis, creating a more comprehensive view of the transaction’s legitimacy.

Verifying Payments

Verifying the authenticity of payments is another crucial function of the UPI UTR number in fraud detection. This verification process involves several key aspects:

- Ensuring Transaction Authenticity

The UTR number acts as a digital fingerprint for each transaction, confirming that the transaction occurred. By verifying the UTR number against the transaction database, financial institutions can ensure that the payment was successfully processed and that the details match the recorded information. - Confirming Recipient Details

The UTR number contains embedded information about the transaction, including recipient details. When a user initiates a transaction, they can verify that the recipient’s details match the intended recipient before confirming the payment. This verification step helps prevent accidental payments to fraudulent or incorrect accounts. - Fraudulent Transaction Detection

In cases of attempted fraud, the UTR number is essential for detecting and rejecting unauthorized transactions. If a transaction does not generate a UTR number due to a failed authentication process, it can be flagged as suspicious. This proactive approach minimizes the risk of fraudulent transactions being completed. - Dispute Resolution

When disputes arise regarding transactions, the UTR number serves as a reference point for resolving the issue. Users can present the UTR number to their bank, which can then access the transaction details and assist in resolving the dispute. This process ensures accountability and transparency, further deterring fraudulent activities. - Real-time Payment Verification

UPI’s real-time payment verification capabilities rely heavily on the UTR number. Financial institutions can verify payments as they occur, ensuring that funds are transferred only when all authentication criteria are met. This real-time verification helps identify and halt fraudulent transactions before they are completed.

UPI UTR Number Format: Structure and Composition

Introduction to UPI and UTR Numbers

Unified Payments Interface (UPI) has revolutionized the way we conduct financial transactions in India. It provides a seamless platform for money transfers, enabling users to send and receive funds instantly using their mobile devices. Each UPI transaction is assigned a unique identifier known as the UTR (Unique Transaction Reference) number. This number is crucial for tracking and managing transactions, ensuring transparency and accountability in digital payments. Understanding the structure and composition of UTR numbers is essential for users and businesses alike, as it helps in identifying transactions and resolving issues.

What is a UTR Number?

A UTR number is a unique identifier that is generated for every UPI transaction. It serves multiple purposes, such as tracking, reconciling payments, and providing reference points in case of disputes. The UTR number is particularly useful for users and merchants who need to verify transactions or address any issues that may arise during the payment process.

Structure of UTR Numbers

The UTR number follows a specific format that consists of a combination of alphanumeric characters. The standard UTR number is 12 characters long and typically includes the following components:

- Bank Code: The first few characters of the UTR number represent the bank or financial institution that processed the transaction. This code is unique to each bank and helps in identifying the source of the transaction.

- Transaction Type Code: The next set of characters indicates the type of transaction. Different codes represent various transaction types, such as fund transfers, bill payments, or merchant payments.

- Date Code: The UTR number also includes a code that signifies the date on which the transaction took place. This is usually represented in a specific format (e.g., YYMMDD), which aids in tracking transactions over time.

- Unique Sequence Number: The final part of the UTR number is a unique sequence that differentiates one transaction from another. This sequence is crucial in preventing duplicate references and ensuring that each transaction can be uniquely identified.

Example of a UTR Number

For instance, a UTR number may look something like this: ICIC200920231234. In this example:

ICICindicates the bank code for ICICI Bank.20might represent the transaction type.092023indicates the date of the transaction, in this case, September 20, 2023.1234is the unique sequence number for that specific transaction.

Composition of UTR Numbers

Alphanumeric Structure

UTR numbers are composed of both letters and numbers. The use of alphanumeric characters helps in creating a more complex and unique identifier, minimizing the chances of duplication. The specific combination of letters and numbers follows the guidelines established by the National Payments Corporation of India (NPCI), which governs UPI transactions.

Length and Format

As mentioned earlier, UTR numbers are generally 12 characters long. However, different banks may have slight variations in their UTR formats. Despite these variations, the fundamental structure remains consistent across the banking system, allowing users to easily recognize and utilize UTR numbers.

Bank-Specific Formats

While the general structure of UTR numbers is standardized, some banks may incorporate their unique identifiers within the UTR format. For example, certain banks may include additional characters to signify specific branches or regions. This can be particularly useful for businesses that operate in multiple locations or for users who frequently engage with different banks.

Importance of UTR Numbers

Tracking Transactions

One of the primary benefits of UTR numbers is their role in tracking transactions. Users can reference the UTR number when checking the status of their payments or when seeking assistance from customer service. This ensures a streamlined process, allowing for quicker resolution of any issues that may arise.

Reconciling Payments

For businesses, UTR numbers are essential for reconciling payments. By matching UTR numbers with invoices or transaction records, businesses can ensure that all payments are accounted for, minimizing the risk of discrepancies in their financial records.

Dispute Resolution

In cases where transactions fail or disputes arise, the UTR number serves as a critical reference point. Users can provide the UTR number to customer support representatives, enabling them to quickly locate and investigate the transaction in question. This enhances the overall user experience and builds trust in the digital payment system.

How to Find Your UTR Number

Finding your UTR number is typically straightforward. Here are some common ways to locate it:

Through Banking Apps

Most banking apps provide users with detailed transaction histories, including UTR numbers. By navigating to the transaction details, users can easily find the UTR number associated with each transaction.

Transaction Notifications

Many banks send transaction notifications via SMS or email, which often include the UTR number. Users can refer to these messages for quick access to their transaction details.

Bank Statements

Users can also find UTR numbers in their bank statements. These statements provide a comprehensive overview of all transactions, including UTR numbers for easy tracking.

Best Practices for Using UTR Numbers

Keep Records

Users and businesses should maintain a record of their UTR numbers for all significant transactions. This practice facilitates easy tracking and reconciliation, especially when dealing with multiple transactions over time.

Share Cautiously

When sharing UTR numbers, users should exercise caution. Providing UTR numbers to unauthorized parties can lead to potential fraud or misuse. Always verify the recipient before sharing sensitive transaction details.

Regular Monitoring

Regularly monitoring transaction histories can help users identify any discrepancies or unauthorized transactions early on. By keeping track of UTR numbers and corresponding transactions, users can quickly address any issues that may arise.

Here’s a detailed guide on what to do if you lose your UPI UTR (Unique Transaction Reference) number, along with steps to retrieve it from your UPI app or bank. This content will be structured in paragraphs for better readability.

What to Do If You Lose the UPI UTR Number?

The Unique Transaction Reference (UTR) number is a vital component of the Unified Payments Interface (UPI) system in India. It acts as a unique identifier for every transaction processed through UPI. Losing your UTR number can be concerning, especially if you need it for tracking, resolving disputes, or for record-keeping purposes. Here’s a comprehensive guide on the steps you can take to retrieve your UTR number, along with tips on ensuring you don’t lose it in the future.

Understanding UTR Numbers

Before delving into the retrieval process, it’s essential to understand what a UTR number is and its significance. A UTR number typically consists of 16 alphanumeric characters, which are assigned to each UPI transaction. This unique code helps banks and users track the status of a transaction, whether it’s successful, failed, or pending. Having access to this number is crucial for resolving any issues related to the transaction, such as refunds or disputes.

Common Reasons for Losing a UTR Number

Several factors can lead to losing your UTR number:

- Accidental Deletion: You might accidentally delete the message or notification containing the UTR number.

- App Issues: Sometimes, UPI apps may have glitches that prevent you from accessing past transaction details.

- Unintentional Forgetting: With multiple transactions, it’s easy to forget specific details like the UTR number.

Steps to Retrieve UTR from UPI App

Most UPI apps, whether it’s Google Pay, PhonePe, Paytm, or your bank’s official app, allow you to view transaction history, including UTR numbers. Here’s how to retrieve it:

- Open Your UPI App: Start by launching the UPI application on your smartphone.

- Go to Transaction History: Look for an option that says ‘Transaction History,’ ‘Recent Transactions,’ or something similar. This section typically lists all your past transactions.

- Locate the Specific Transaction: Scroll through the list to find the specific transaction for which you need the UTR number. You can often filter the transactions by date or amount to make the search easier.

- View Transaction Details: Once you find the desired transaction, tap on it to view more details. The UTR number is usually displayed along with other details like the transaction amount, date, time, and status.

- Save the UTR Number: After locating the UTR number, consider saving it in a secure location, such as a note-taking app, or taking a screenshot for future reference.

Steps to Retrieve UTR from Bank

If you cannot find the UTR number through your UPI app, you can retrieve it by contacting your bank directly. Here’s how:

- Contact Customer Support: Call or visit the nearest branch of your bank. You can also use the bank’s official website or app to find contact information for customer support.

- Provide Necessary Information: When contacting customer support, be prepared to provide details about the transaction, including the transaction date, amount, and recipient’s information. This information will help the representative locate your transaction.

- Request the UTR Number: Ask the representative to provide you with the UTR number associated with your transaction. They may need to verify your identity, so have your account information ready.

- Check Email or SMS Notifications: Banks often send transaction notifications via email or SMS. Check your registered email or messages for any transaction confirmation, which usually contains the UTR number.

- Online Banking Portal: If your bank offers online banking, log in to your account and navigate to the transaction history section. Similar to the UPI app, you should be able to find the UTR number listed with the transaction details.

Additional Tips to Avoid Losing UTR Numbers

To prevent future issues with losing your UTR number, consider the following practices:

- Keep a Record: Maintain a dedicated folder in your email or a secure note-taking app for all UPI transactions. This way, you can easily retrieve UTR numbers when needed.

- Screenshots: After completing significant transactions, take a screenshot of the confirmation page that includes the UTR number.

- Use a Password Manager: If you’re concerned about security, consider using a password manager that allows you to store sensitive information securely.

- Regularly Check Transaction History: Make it a habit to review your transaction history periodically, so you’re familiar with the details of your recent transactions.

- Enable Notifications: Ensure that notifications for your UPI app are enabled, so you receive updates about your transactions, including UTR numbers.

Common Issues Related to UPI UTR Numbers

Unified Payment Interface (UPI) has revolutionized the way we conduct financial transactions in India, making them faster and more convenient. At the heart of these transactions lies the Unique Transaction Reference (UTR) number, which serves as a crucial identifier for each payment made through the UPI system. However, users often encounter issues related to UTR numbers that can lead to confusion and complications. Two common issues are the non-generation of UTR numbers and mismatches in payment records. Understanding these issues is essential for users to navigate the UPI landscape effectively and ensure that their transactions are processed smoothly.

UTR Not Generated

One of the primary issues that UPI users may encounter is the non-generation of a UTR number after a transaction attempt. This situation can arise for several reasons, and it can lead to frustration for users who rely on timely and reliable payment processing.

Technical Glitches

The UPI system, like any digital platform, is subject to technical glitches. These glitches may occur due to server downtime, network issues, or problems with the banking infrastructure. When users attempt to make a payment, any disruption in the UPI system can prevent the generation of a UTR number. In such cases, the transaction may appear to be pending or unsuccessful, leaving the user unsure about the status of their payment. It is essential to verify the transaction status through the UPI app or bank statement, as the funds might still be deducted without the UTR being generated.

User Errors

Sometimes, users may inadvertently make errors while initiating a transaction. These errors can range from incorrect input of payment details to insufficient balance in their bank account. If a transaction fails due to user error, the UTR number will not be generated. Users should always double-check the recipient’s details, such as the mobile number or VPA (Virtual Payment Address), and ensure they have adequate funds before proceeding with the payment. Learning to navigate the UPI app efficiently and understanding common pitfalls can help minimize these errors.

Bank Policies and Limitations

Each bank may have specific policies regarding UPI transactions, including limits on transaction amounts and the number of transactions allowed within a specific time frame. If a user attempts to exceed these limits, the bank may block the transaction and, consequently, not generate a UTR number. Users should familiarize themselves with their bank’s UPI policies to avoid such situations. Contacting the bank’s customer service can provide clarity on any imposed limits and help users make informed decisions.

UPI App Issues

The app used for making UPI transactions can also be a source of problems. Outdated versions of the app may have bugs that interfere with transaction processing. It is advisable for users to keep their UPI applications updated to the latest version to ensure optimal performance. Additionally, cache and data buildup in the app can lead to operational issues, which can be resolved by clearing the app’s cache or reinstalling it. Regular maintenance of the app is essential for a smooth user experience.

Resolution Steps

In the event that a UTR number is not generated, users should first check the transaction history in their UPI app. If the transaction appears as successful but no UTR is generated, they should contact customer support for their UPI app or bank to inquire about the transaction status. Providing them with details such as the date, time, and amount of the transaction can facilitate a quicker resolution. Additionally, users should monitor their bank statements to ensure that no unauthorized deductions have occurred.

Mismatched UTR in Payment Records

Another common issue related to UPI transactions is the mismatch of UTR numbers in payment records. This situation can arise when users notice discrepancies between their transaction history in the UPI app and the records maintained by the bank or the recipient.

Data Synchronization Issues

One of the primary reasons for mismatched UTR numbers is the synchronization issues between different platforms. When a transaction is initiated, multiple systems are involved in processing the payment, including the UPI app, the banks of both the sender and recipient, and the National Payments Corporation of India (NPCI). If there are delays in updating records across these systems, it can lead to discrepancies in the UTR numbers. Users may see a different UTR in their bank statement compared to what is shown in the UPI app.

Manual Entry Errors

In some cases, users might manually enter UTR numbers while reconciling their records, leading to mismatches. This is especially common in business scenarios where multiple transactions are processed. Human error during data entry can result in the wrong UTR being recorded or noted, causing confusion when trying to trace a specific transaction. Implementing standardized processes for recording UTR numbers and regularly cross-referencing with digital records can help reduce such errors.

Delayed Transactions

Sometimes, transactions may be delayed, leading to users believing that a payment has not been completed when, in fact, it has been processed. In such scenarios, the UTR may appear in the bank records at a different time than expected. Users should maintain a record of transaction dates and times to match with the bank’s statements accurately. If a payment is confirmed but does not reflect correctly, contacting customer service for clarification is advisable.

Fraudulent Activities

Mismatched UTR numbers can also raise concerns about fraudulent activities. If users notice a UTR number they do not recognize or if the UTR linked to a specific transaction appears different in the recipient’s records, it may indicate unauthorized transactions. Users should be vigilant about such discrepancies and report any suspicious activity to their bank immediately. Regular monitoring of transaction history and alert settings can help detect fraud early.

Resolution Steps

To resolve issues related to mismatched UTR numbers, users should first gather all relevant details, including transaction amounts, dates, and UTR numbers from both their UPI app and bank records. Comparing this information can help identify where the discrepancies lie. In cases where the mismatch persists, reaching out to customer support for both the UPI app and the bank is crucial. They can assist in reconciling the records and provide insight into any potential issues within their systems.

Conclusion

In conclusion, while UPI has significantly enhanced the ease of conducting financial transactions in India, issues related to UTR numbers, such as non-generation and mismatches in payment records, can create confusion for users. Understanding the common causes of these problems and implementing best practices for transaction management can help mitigate their impact. Users should remain proactive in monitoring their transaction histories, ensuring they use updated applications, and familiarizing themselves with their bank’s UPI policies. By doing so, they can enjoy a more seamless and reliable payment experience through UPI, minimizing the chances of encountering UTR-related issues.